The Federal Trade Commission is taking action against personal finance app provider Brigit, alleging that its promises of “instant” cash advances of up to $250 for people living paycheck-to-paycheck were deceptive and that the company locked consumers into a $9.99 monthly membership they couldn’t cancel.

Brigit, also known as Bridge It, Inc., has agreed to settle the FTC’s charges, resulting in a proposed court order that would require the company to pay $18 million in consumer refunds, stop its deceptive marketing promises, and end tactics that prevented customers from cancelling.

“Brigit trapped those consumers least able to afford it into monthly membership plans they struggled to escape from,” said Sam Levine, Director of the FTC’s Bureau of Consumer Protection. “Companies that offer cash advances and other alternative financial products have to play by the same rules as other businesses or face potential action by the FTC.”

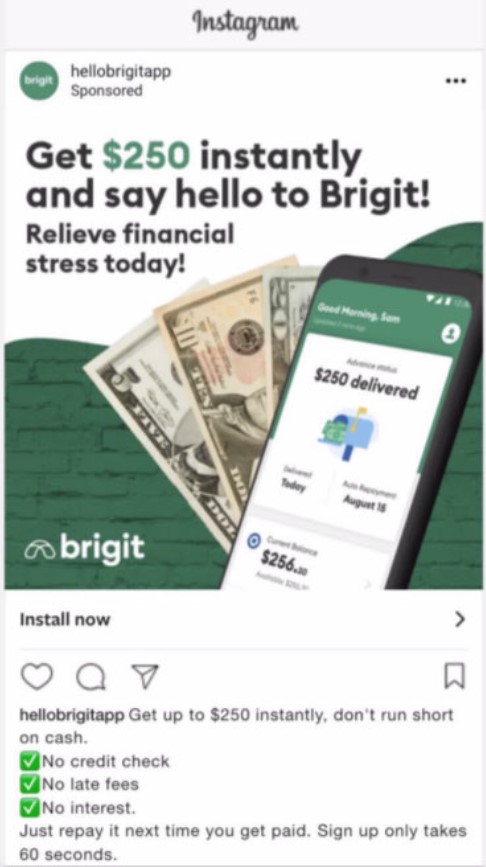

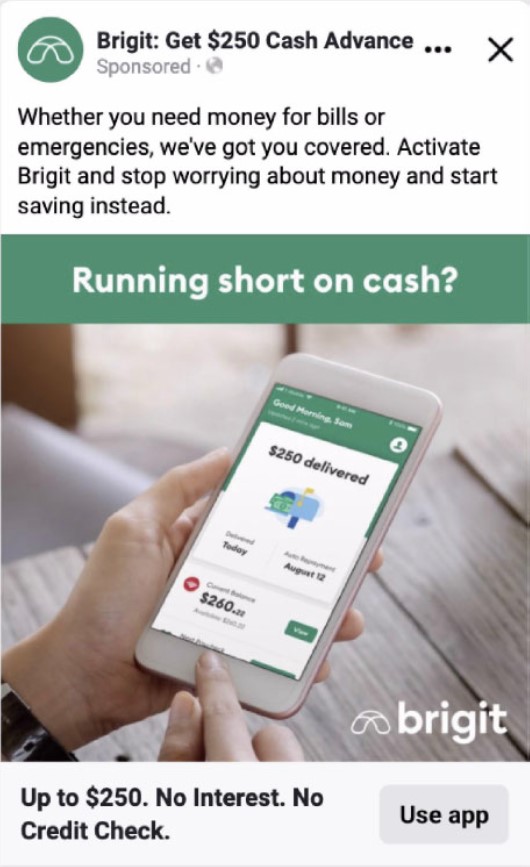

According to the FTC’s complaint, Brigit advertised its cash advance service online, through social media and through broadcast ads with claims that customers who subscribed to the company’s service would have access to “instant” cash advances of up to $250 “whenever you need it,” and could cancel anytime. Consumers could only access the cash advance features when they signed up for the $9.99 per month “Plus” subscription.

The FTC’s complaint, however, charges that consumers were rarely able to get an advance for the promised $250, and in many cases consumers were not able to receive a cash advance at all. Despite Brigit’s promises that advances would be available with “free instant transfers,” the complaint notes that the company began charging consumers a 99 cent fee for an instant transfer. Consumers who did not pay the fee had to wait up to three business days for their advances.

In addition, the complaint charges that while Brigit claimed to offer “non-recourse” advances with no fees or interest, the company prevented consumers who had an open advance from cancelling their subscription and continued to withdraw $9.99 monthly from their bank account until the advance was paid off. Such monthly charges created significant additional hardship for consumers already struggling to pay off a cash advance.

Even when consumers without an open cash advance attempted to cancel the paid subscription, the complaint charges that the company employed dark patterns—manipulative design tricks—to create a confusing and misleading cancellation process that prevented consumers from cancelling their subscriptions, instead of offering a simple mechanism to cancel, as required by the Restore Online Shoppers’ Confidence Act (ROSCA).

The proposed settlement order, which must be approved by a federal judge before it can go into effect, would require Brigit to pay $18 million to the FTC to be used to provide refunds to consumers. In addition, the order would prohibit Brigit from misleading consumers about how much money is available through their advances, how fast the money would be available, any fees associated with delivery, and consumers’ ability to cancel their service. The order would also require the company to make clear disclosures about its subscription products and provide a simple mechanism for consumers to cancel.

The Commission vote authorizing the staff to file the complaint and stipulated final order was 3-0. The FTC filed the complaint and final order in the U.S. District Court for the Southern District of New York.

NOTE: The Commission files a complaint when it has “reason to believe” that the named defendants are violating or are about to violate the law and it appears to the Commission that a proceeding is in the public interest. Stipulated final orders have the force of law when approved and signed by the District Court judge.

The staff attorneys on this matter were Patrick Roy, Mark Glassman and James Doty of the FTC’s Bureau of Consumer Protection.